I almost signed a contract once that would have cost me $28,000. It was early in my export career, and a broker had connected me with a large buyer in the Middle East. The contract was 14 pages of dense legal English, and I was too eager to close the deal to read it properly. I flipped to the price, checked the volume, and reached for the pen. My wife, who is not a lawyer but has better instincts than I do, stopped me. "Read the quality rejection clause," she said. I read it. Buried in paragraph 11.3 was a sentence stating that any quality dispute would be resolved solely by a laboratory nominated by the buyer, with the cost borne by the seller, and the buyer could reject the entire container without a third-party verification. If I had signed that contract, one questionable cupping report could have authorized the rejection of a full container load, leaving me with the freight cost, the return shipment cost, and 19 tons of coffee stranded in a foreign port. That near miss fundamentally changed how I evaluate contracts.

The top five red flags in a coffee supplier contract are unilateral quality rejection clauses that lack third-party verification, vague force majeure language that the supplier can invoke for routine business problems, the absence of a volume tolerance band that acknowledges agricultural variability, payment terms that demand full prepayment without a performance guarantee, and exclusive jurisdiction clauses that force dispute resolution in the supplier's local courts, all of which shift an unfair share of risk onto the buyer.

A coffee supply contract is not just a document of commercial terms. It is a risk-allocation instrument. Every clause distributes a specific risk—of crop failure, of quality degradation, of currency fluctuation, of political intervention—between the two parties. A fair contract distributes these risks reasonably. An unfair contract loads them onto one party, usually the buyer, and disguises the imbalance in legal language that sounds neutral. Over the years, I have reviewed contracts from both sides of the table, as a buyer of agricultural inputs and as a seller of green coffee. I want to share the five red flags I now look for immediately, the ones that genuinely predict whether a supplier relationship will survive a difficult season or collapse acrimoniously.

Why Is a Unilateral Quality Rejection Clause a Serious Contract Risk?

Quality rejection is the nuclear option in a coffee contract. It means the buyer claims the beans do not meet the agreed specifications and refuses to accept them. The financial consequence for the seller is catastrophic—lost product, lost freight costs, and a damaged reputation. Because the stakes are so high, the mechanism for determining whether a rejection is valid must be objectively balanced. A unilateral rejection clause destroys that balance. It gives one party the sole power to decide whether the quality is acceptable, and that party is almost always incentivized to find defects if the market price has dropped since the contract was signed.

A unilateral quality rejection clause is a contract risk because it allows the buyer to declare a quality default without an independent third-party verification, creating a commercial incentive to reject shipments opportunistically when the spot market price falls below the contract price, essentially turning a quality protection mechanism into a free option to walk away from the deal.

I have seen this play out in real life through a colleague's experience. He shipped a container of specialty-grade Arabica at a contract price of $3.40 per pound. Between the contract date and the delivery date, the C-market dropped sharply, and the spot price for similar quality fell to $2.90. The buyer, invoking a unilateral rejection clause, claimed the coffee did not meet the cup score requirement. My colleague had no right to a third-party verification. The buyer nominated their own cupper, who unsurprisingly found the coffee to be 1.5 points below the spec. The container was rejected. My colleague was forced to sell the spot at $2.95, losing $0.45 per pound on a 42,000-pound container—a total loss of nearly $19,000. The beans were actually perfectly fine. The rejection was a market-timing exercise disguised as a quality complaint. A fair contract prevents this by requiring third-party verification from an SCA-certified lab that both parties agree to in advance, with the lab's report being binding on both sides. If a contract does not have this third-party mechanism, or if the verification body is exclusively chosen by one party, the buyer is exposed to a risk that may never materialize in a stable market but becomes acute the moment prices swing. For any buyer reviewing a supplier contract, this is the first clause I recommend reading, and reading slowly.

How should a balanced quality determination process be structured in a contract?

A balanced quality determination process has four essential components. First, the contract must specify the exact grading protocol that will be used—usually the Specialty Coffee Association Green Grading Protocol and Cupping Protocol, referenced by their specific version year. Second, the contract must name a specific, independent third-party inspection company that both parties have pre-approved, such as SGS, Bureau Veritas, or a named coffee-specific surveyor. Third, the contract must state that the sampling for the quality determination will be conducted by this third party according to the SCA sampling standard, not by the buyer unilaterally. Fourth, the contract must state that the third party's report is binding on both parties, meaning neither the buyer nor the seller can dispute it further through other channels.

The process typically follows this sequence: upon container arrival, the buyer has a specified window—I use 72 hours in my contracts—to notify the seller of a quality concern. Within that window, the buyer requests the named third party to draw a representative sample from the container and conduct a full SCA physical and sensory analysis. The seller is notified and may be present during the sampling if they wish. The third party's report is delivered to both parties simultaneously. If the report confirms the beans are out of spec, the buyer has the right to reject the lot, and the seller bears the return freight and related costs. If the report confirms the beans are within spec, the buyer must accept the lot and any quality complaint is considered resolved. This structure eliminates the incentive to use quality rejection as a market-timing tool. The buyer knows that a frivolous complaint will be exposed by the independent report, and the seller knows that a genuine quality failure will be confirmed objectively. For a buyer, seeing this kind of structured, balanced quality determination in a supplier's contract is actually a positive signal, not a red flag, because it shows the supplier is confident enough in their product to submit it to independent scrutiny.

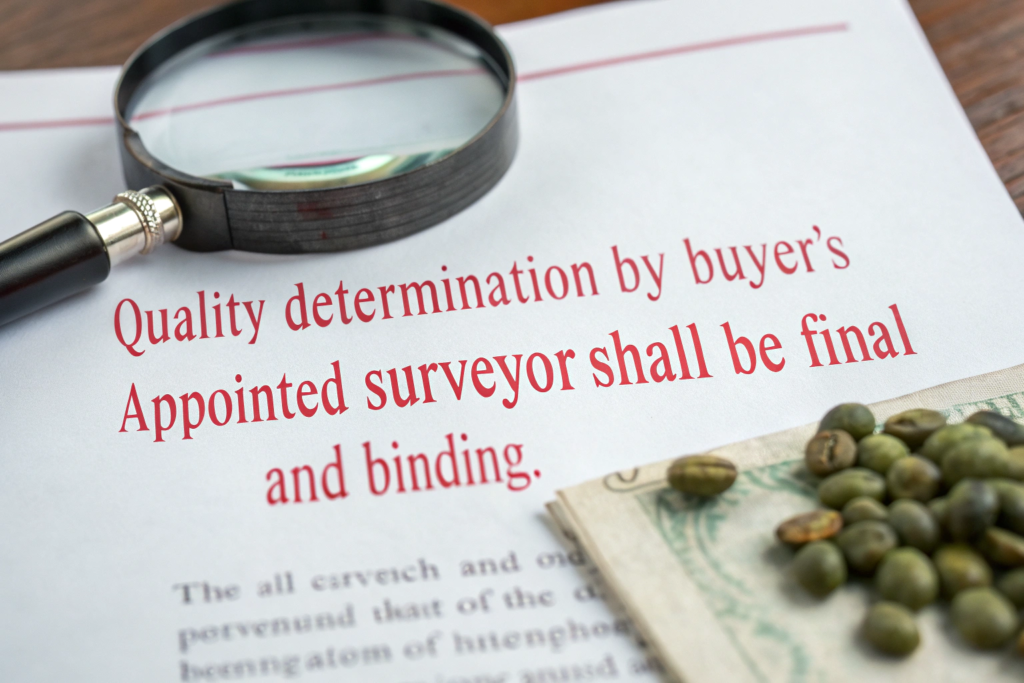

What is the difference between "final and binding" and "conclusive evidence" wording?

This is a technical but important distinction in contract law. The phrase "final and binding" means the decision of the named party—say, a surveyor—is the end of the matter. It cannot be appealed, challenged, or revisited through litigation or arbitration. If a contract says the buyer's internal cupping report is "final and binding," the seller has completely surrendered their right to contest a rejection, even if the rejection is factually wrong. This wording is a major red flag.

"Conclusive evidence" is a slightly different concept. It means the document—the survey report—will be treated as proof of the facts it contains in any subsequent legal proceeding, but it does not necessarily preclude a challenge to the process by which that evidence was obtained. A contract that says a third-party SGS report is "conclusive evidence of quality" still provides some procedural protection, because the report originates from an independent entity and the methodology is standardized. The gold standard, however, is a combination: a contract that specifies that the report of a named, independent third party shall be "final and binding" on both parties. This provides certainty and eliminates the possibility of either party dragging a quality dispute through arbitration for months after the coffee has already degraded. When I review a contract, I scan for the word "final" and immediately check who is empowered to make the final determination. If it is one party unilaterally, the contract is unbalanced. If it is a named independent third party, the contract is built on a model that international commodity traders have used for decades.

How Can Vague Force Majeure Language Be Exploited by Unreliable Suppliers?

Force majeure is a necessary clause in any agricultural supply contract. It protects both parties when an unforeseeable, extraordinary event outside their control prevents them from fulfilling their obligations. The classic triggers are war, natural disasters, pandemics, and government-mandated restrictions. The clause is supposed to be a shield against genuine catastrophes. In the hands of an unreliable supplier, however, a poorly drafted force majeure clause becomes a sword to escape contractual obligations when the market moves against them or when their own poor planning causes a supply shortfall.

Vague force majeure language becomes exploitable when it includes broad, non-specific phrases like "any other event beyond the seller's reasonable control" without an accompanying list of specific exclusions, allowing a supplier to declare force majeure for foreseeable commercial difficulties such as a rise in cherry prices, a trucking delay, or a quality shortfall from their own processing errors, none of which are true force majeure events.

I have seen a supplier declare force majeure because "adverse weather conditions" reduced the harvest yield. When I asked for the specific weather data, it turned out the rainfall was within the normal historical range for that region. The supplier had simply over-sold their crop and was using a generic weather excuse to reduce their delivery obligation. A well-drafted force majeure clause would require the party invoking it to provide objective evidence of the event—a government weather report showing rainfall exceeding the ten-year standard deviation, or a meteorological bureau declaration of a drought. The clause should also require the party to prove that the event specifically prevented the fulfillment of this contract, not just that it created a general inconvenience. Without these evidentiary requirements, force majeure becomes a convenient escape hatch. For the buyer, the loss is not just the specific shipment. It is the production gap, the unrecovered roasting schedule, and the damage to their own downstream customer commitments. A vague force majeure clause transfers all of this business risk onto the buyer while giving the supplier a cost-free exit.

What specific events should a force majeure clause explicitly list and exclude?

A strong force majeure clause lists the qualifying events with precision and, equally importantly, lists the events that do not qualify. The qualifying events are the standard catastrophes: war, civil war, rebellion, revolution, insurrection, military action, terrorism, nuclear accident, earthquake, volcanic eruption, tsunami, cyclone, hurricane, epidemic or pandemic as declared by the World Health Organization, and government-mandated export prohibition specifically applying to the commodity and origin in question.

The excluded events are where the clause earns its protective value. The exclusions should explicitly state that force majeure does not include changes in market price or the cost of raw materials, the supplier's inability to source coffee from their own upstream farmers at a profitable price, labor strikes limited to the supplier's own facility, breakdown of the supplier's own machinery that could have been prevented by routine maintenance, delays in inland transportation caused by the supplier's chosen logistics provider, and any event that the supplier could have reasonably foreseen and mitigated through prudent business planning. I include these exclusions in our own force majeure clause because I want the buyer to know that I am not using the clause as a commercial escape route. If I genuinely cannot ship because the government has closed the port of Shanghai due to a public health emergency, the clause protects me, and the buyer understands that. If I simply paid too much for cherry and the contract price is now underwater, the clause does not protect me, and the buyer is right to demand performance. The specificity of the excluded events is what distinguishes a force majeure clause that builds trust from one that invites abuse.

How can the buyer verify a force majeure claim in real time?

Real-time verification of a force majeure claim is essential because the buyer is often thousands of miles away from the claimed event. If a supplier in Yunnan claims the road to the port is blocked by a landslide, the buyer in Chicago has no direct way to verify that claim. The contract must therefore build in a verification mechanism. The clause I use requires the supplier to provide, within seven calendar days of notifying force majeure, a package of supporting evidence. For a weather event, this includes a certified report from the provincial meteorological bureau with specific rainfall or wind speed data. For a government restriction, this includes a copy of the official government order with an English translation. For a strike at a port, this includes a notice from the port authority confirming the operational closure.

The contract should also give the buyer the right to commission an independent verification at their own cost. If the buyer suspects the force majeure claim is fabricated, they can instruct a local surveyor—there are international inspection companies with offices in Shanghai and Kunming—to visit the affected area and report on the actual conditions. The cost of this independent verification is borne by the party whose position is found to be incorrect. If the surveyor confirms the landslide is real, the buyer pays the survey cost. If the surveyor reports the road is open and functioning normally, the supplier pays the survey cost and the force majeure claim is void. This mechanism deters false claims because the supplier knows a fraudulent declaration will be exposed and will cost them money and credibility. For a buyer entering a new relationship with a Chinese supplier, the presence of a force majeure verification clause is a strong signal of the supplier's genuine intention to perform, not to find excuses.

Why Does the Absence of a Volume Tolerance Band Signal a Misunderstanding of Agriculture?

Coffee is not manufactured in a factory. It is grown on trees that are subject to rainfall, temperature, pest pressure, and the biennial bearing cycle that causes alternating high-yield and low-yield years. A contract that specifies a fixed volume—say, exactly 19.2 metric tons per quarter for two years—without any tolerance band is a contract that pretends coffee is a widget. When the harvest inevitably fluctuates, that contract will break. The supplier will either short-ship and face a breach claim, or they will source beans from outside their own farm to fill the volume, potentially degrading the quality and authenticity of the lot.

The absence of a volume tolerance band is a red flag because it signals that the supplier either does not understand the agricultural reality of coffee production, or understands it but is willing to sign a commitment they know they may not be able to honor, pushing the inevitable shortfall problem into a future dispute rather than addressing it transparently at the contracting stage.

A volume tolerance band, typically expressed as plus or minus 10% or 15% of the contracted volume, with the final volume to be confirmed 30 days before shipment, is not a concession to supplier laziness. It is an honest acknowledgment of agricultural variability. The band gives the buyer time to plan—if the shipment will be 10% short, the buyer has four weeks to source the balance from another supplier or adjust their production schedule. The band also protects the buyer from being forced to accept more coffee than their warehouse or cash flow can absorb, because the upper bound limits the supplier's ability to push excess inventory. Contracts without this band tend to produce one of two outcomes: the supplier quietly blends in cheaper external beans to meet the exact volume, or the supplier defaults at the last minute and leaves the buyer scrambling. Neither outcome builds a long-term supply relationship.

How should a volume flexibility clause be linked to a harvest forecast schedule?

The volume flexibility clause works best when it is tethered to a harvest forecast schedule that the supplier shares with the buyer throughout the growing season. The schedule starts with a flowering report, usually available about six months before the harvest. The flowering report gives an initial indication of the crop size. If flowering was sparse, the supplier can already flag that the harvest may come in at the lower end of the tolerance band. The second report is the cherry development assessment, about three months before harvest, when the green cherries are visible on the trees and a yield estimate per hectare can be calculated with reasonable accuracy. The third report is the harvest progress update, issued mid-harvest, which tracks the actual cherry volumes being delivered to the wet mill.

Each report gives the buyer progressively more information. By the time the 30-day final notice is issued, the volume adjustment, if any, should not be a surprise. The buyer has had months of advance warning that the crop is trending light or heavy. This harvest forecast schedule is not difficult to produce. On our own plantation, we generate these reports as part of our standard agronomy management. Sharing them with contract buyers costs us nothing and prevents the kind of last-minute volume notification that feels like a breach, even when it is technically within the tolerance clause. A supplier who is unwilling to share harvest forecasts throughout the season may be managing a supply chain that is not fully under their own control—they may be aggregating from multiple small farmers and genuinely do not know their final volume until the last bag is milled. That is a different risk profile than a plantation owner who can monitor flowering across their own acreage. For a buyer seeking a long-term supply partner, the willingness to share harvest forecasts is a transparency indicator that correlates strongly with contract performance.

Can a fixed-volume contract work if the supplier holds a buffer stock?

A fixed-volume contract can work, but only if the supplier explicitly commits to maintaining a buffer stock to absorb production variability, and the contract specifies the buffer stock mechanism. A buffer stock is a reserve of green coffee from the previous harvest, stored under controlled conditions, that is held specifically to cover contractual shortfalls. Without this buffer, a fixed-volume contract is simply a hope dressed up as a legal document.

The buffer stock mechanism adds cost for the supplier—they are tying up working capital in inventory that cannot be sold on the spot market—so a supplier who offers a genuine buffer-backed fixed-volume contract will typically price it slightly higher to reflect the cost of maintaining the reserve. This is a premium worth paying. My advice to a buyer who is offered a fixed-volume contract at a standard market price with no buffer clause is to be skeptical. The economics do not work. The supplier is either cutting corners on quality, planning to source from the open market to cover shortfalls, or has not thought through the implications of a bad harvest. In any of these scenarios, the fixed-volume promise is unreliable. A contract that honestly prices the buffer stock into the unit cost and specifies the buffer storage conditions and the independent inspection rights is the only form of fixed-volume agreement that a buyer should treat as a genuine commitment.

How Do Full Prepayment Terms Without a Guarantee Expose the Buyer to Total Loss?

Payment terms are the point where trust and risk intersect with the greatest intensity. In the coffee export trade, it is not uncommon for suppliers to request a significant prepayment—30%, 50%, or even 100%—before the coffee is shipped. The supplier's perspective is understandable. They are committing their inventory, or their upcoming harvest, to a specific buyer. If the buyer defaults, the supplier is left holding a container load of coffee with a specific quality profile that may not be easily remarketed at the same price. Prepayment protects the supplier against buyer default. But an unprotected full prepayment exposes the buyer to an equally severe risk: the supplier takes the money and does not ship the coffee.

Full prepayment terms without a corresponding performance guarantee—such as a standby letter of credit issued by the supplier's bank, export credit insurance, or a structured escrow arrangement—expose the buyer to the risk of total financial loss, as there is no mechanism to recover the funds if the supplier fails to ship, ships substandard beans, or ships beans that do not match the contract specifications.

I do not ask my buyers for full prepayment. I ask for a 30% deposit at contract signing and the 70% balance against scanned shipping documents—the bill of lading, the phytosanitary certificate, the insurance certificate, and the pre-shipment sample cupping report. This structure gives me enough working capital to cover harvest and processing costs for that specific lot, while giving the buyer the security of paying the bulk of the purchase price only when they have documentary evidence that the coffee exists, has been loaded onto a vessel, and meets the quality specifications. For a first-time buyer relationship, I sometimes suggest starting with a smaller trial shipment and full payment against documents, so both parties build confidence incrementally. A supplier who demands 100% prepayment from a new buyer without a performance guarantee is asking the buyer to assume a risk that the supplier themselves is unwilling to bear—the risk of counterparty default. This asymmetry is a significant red flag.

What is a standby letter of credit and how does it safeguard a prepayment?

A standby letter of credit, often abbreviated as SBLC, is a guarantee issued by the supplier's bank. It is a document that says, in effect, "if our client fails to perform their contractual obligations, we, the bank, will pay the beneficiary—the buyer—a specified amount." The standby LC is separate from the commercial letter of credit used for payment. It is an insurance policy. If the supplier takes the 30% prepayment and then fails to ship the coffee by the agreed date, the buyer presents a simple demand to the bank, along with evidence that the supplier defaulted, and the bank pays out the prepaid amount. The supplier's account is then debited by the bank, so the supplier is strongly incentivized not to default.

For a supplier, obtaining a standby LC requires a credit line with their bank and incurs a small issuance fee, typically 1% to 3% of the guaranteed amount per year. A supplier who is unwilling or unable to provide a standby LC for a large prepayment is signaling either that their banking relationships are weak—which is a financial stability concern—or that they are not confident enough in their own ability to perform to put a bank guarantee behind their promise. For a buyer considering a substantial prepayment to a new supplier, requesting a standby LC is a reasonable risk management step. If the supplier refuses, the buyer should either negotiate different payment terms or walk away from the deal.

How can an escrow service work for smaller coffee purchase transactions?

For smaller transactions—say, a micro-lot purchase of a few thousand dollars rather than a container load—a full letter of credit or standby LC may be impractical due to bank fees and minimum transaction sizes. An escrow service provides a simpler, lower-cost alternative. An escrow is a trusted third party, often an online platform specializing in international trade, that holds the buyer's payment in a segregated account. The funds are not released to the supplier until the buyer confirms receipt of the goods and their satisfaction with the quality.

The process works in three stages. First, the buyer deposits the agreed purchase price into the escrow account. The escrow service confirms to the supplier that the funds are secured. Second, the supplier ships the coffee and uploads the shipping documents to the escrow platform. The buyer tracks the shipment. Third, upon delivery, the buyer has an inspection period—typically five to seven calendar days—to inspect the beans and confirm acceptance. If the buyer confirms, the escrow service releases the funds to the supplier. If the buyer rejects the lot based on documented quality issues, the dispute resolution process defined by the escrow service is triggered, and the funds are held until the dispute is resolved or returned to the buyer. For a first-time transaction between a buyer and a Chinese coffee supplier, I recommend escrow as a bridge of trust. It protects both parties. The supplier knows the money exists and is committed. The buyer knows the money is safe until the coffee is delivered as promised.

Conclusion

A coffee supply contract is a document of risk allocation, and the five red flags I have described—unilateral quality rejection, vague force majeure, absent volume tolerance bands, unprotected full prepayment, and exclusive home-court jurisdiction—are all mechanisms that shift risk unfairly onto the buyer while protecting the supplier from the consequences of their own failures. A contract that contains one of these red flags may still perform adequately in a stable market with a supplier who operates in good faith. But contracts exist for the moments when markets are not stable and good faith is tested. A contract with multiple red flags is not a contract. It is an option for the supplier to perform if it suits them and walk away if it does not.

The good news is that every one of these red flags has a corresponding fair alternative. Third-party quality verification replaces unilateral rejection. Specific event lists and verification mechanisms replace vague force majeure. Volume tolerance bands with harvest forecasts replace rigid volume commitments. Standby letters of credit or escrow replace unprotected prepayment. Neutral arbitration replaces exclusive home-court jurisdiction. These fair alternatives are standard in international commodity trade. They are not novel or experimental. A supplier who builds their contract on these balanced foundations is a supplier who is looking for a partnership that endures across market cycles.

If you are a roaster, importer, or distributor who has encountered these red flags in supplier contracts, or if you are reviewing a contract from a potential Chinese coffee partner and want a second opinion on the terms, we at BeanofCoffee are open to that conversation. Our contracts are built on the balanced principles I have described, and our export director, Cathy Cai, can provide a sample contract for your review, along with our quality rejection procedure, force majeure verification template, and our standard SIAC arbitration clause. Contact Cathy directly at cathy@beanofcoffee.com. Let us work together on a supply agreement where the contract itself is a foundation for trust, not a source of hidden risk.